What Is Document Authentication and Why Does Your Bank Need It?

Financial institutions face unprecedented fraud threats as cybercriminals deploy sophisticated techniques, including deepfakes and synthetic identities. Document authentication verifies identity document legitimacy through optical character recognition, biometric analysis, and artificial intelligence. Banks implementing robust customer identification program protocols reduce fraud exposure while maintaining regulatory compliance.

The document authentication process combines multiple verification methods to detect counterfeit documents before fraudulent accounts are established. Modern systems analyze microprint, holograms, and machine-readable zones while comparing document data against biometric markers. This multimodal approach addresses global scam losses reaching USD 1.03 trillion annually, requiring technology solutions that outpace criminal innovation.

Key Takeaways

- Document authentication uses OCR and template matching to verify the legitimacy of identity documents

- Synthetic identity fraud costs financial services USD 30-35 billion annually

- Facial recognition accuracy exceeds 99.97% in ideal conditions

- Every USD 1 invested in fraud prevention prevents USD 3-5 in losses

- The global identity verification market will reach USD 29.32 billion by 2030

What Is Document Authentication?

Document authentication is the systematic verification of physical or digital identity documents to confirm legitimacy and prevent fraud. This process extracts embedded information from passports, driver's licenses, and government-issued IDs to validate authenticity. Banks rely on automated authentication systems to screen millions of documents while reducing manual review time by up to 90%.

Authentication systems create digital fingerprints by analyzing security features invisible to human reviewers. These fingerprints are compared against templates of legitimate documents from thousands of issuing authorities worldwide. The technology identifies discrepancies in font spacing, material composition, and embedded security elements, distinguishing genuine documents from sophisticated counterfeits.

How Does Document Authentication Work?

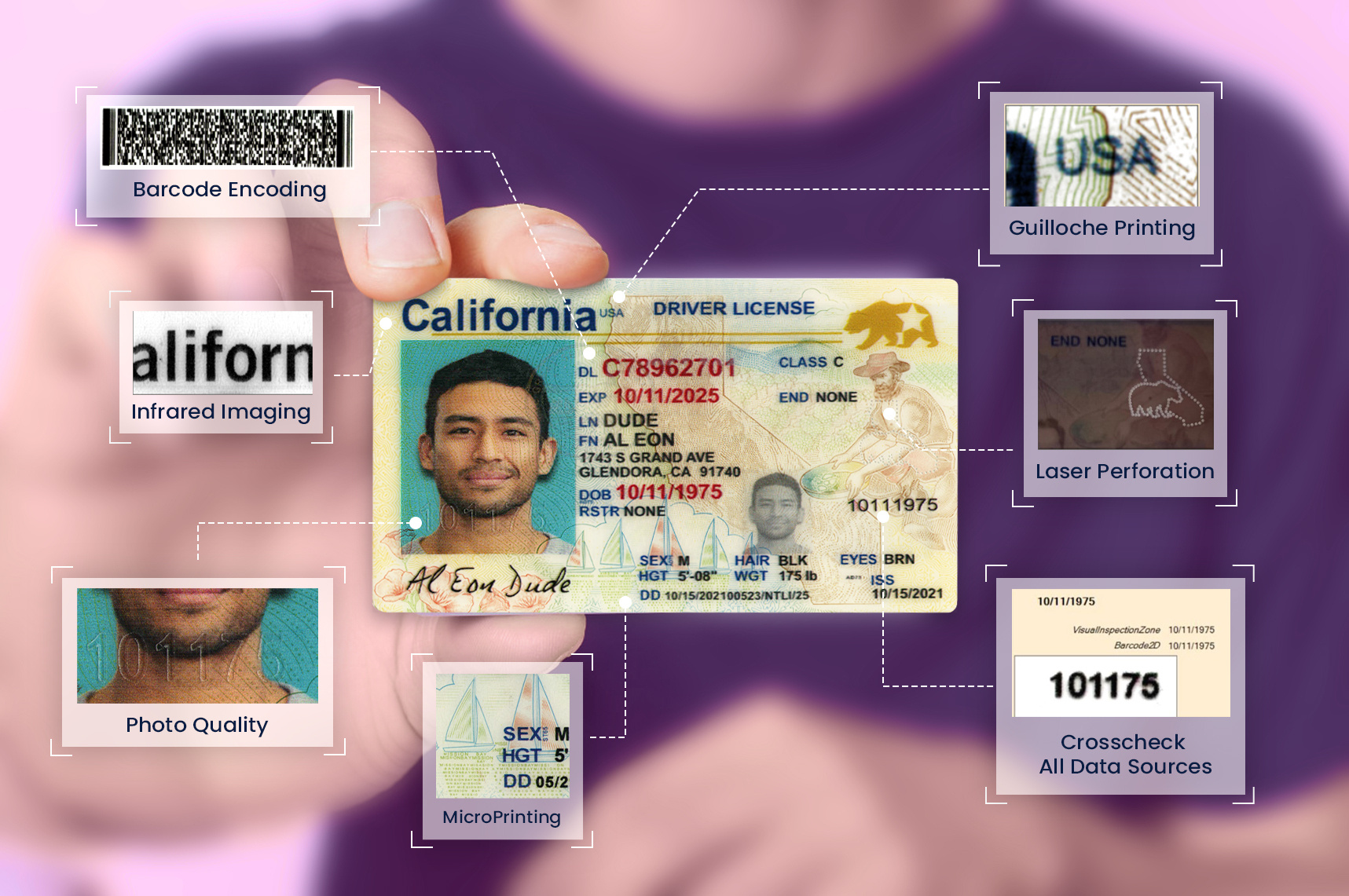

OCR extracts text from physical documents and analyzes microprint to detect alterations or fabrications. Systems check holograms and verify machine-readable zones using standardized formats. MRZ is a standardized area on identity documents containing encoded biographical and document data readable by automated systems.

Template matching verifies document legitimacy by comparing submissions against databases of authentic specimens from issuing governments. Advanced systems analyze paper texture through high-resolution imaging to identify differences between genuine security paper and standard printing stock. This multi-layered approach ensures ID authentication meets the highest standards for institutions facing regulatory scrutiny.

What Technologies Are Used for Document Authentication?

Facial recognition algorithms map facial geometry by measuring distances between key facial landmarks, including eye spacing and nose position. AI systems utilize machine learning for pattern recognition, analyzing thousands of document features simultaneously. Real-time anomaly identification through behavioral analysis flags inconsistencies between document data and user-provided information.

Facial recognition accuracy exceeds 99.97% in ideal conditions with consistent lighting and adequate resolution. AU10TIX provides 4-8 second automated document authentication by processing images through neural networks trained on millions of verified specimens. This speed enables banks to authenticate customers during account opening without creating friction that drives abandonment.

What Types of Documents Are Typically Verified?

Banks verify government-issued passports containing machine-readable zones with embedded biographical data and digital photographs. Driver's licenses from all 50 states and Canadian provinces undergo authentication to prevent identity theft during account opening. National identity cards, resident alien cards, and military identification documents are processed through the same authentication pipelines.

Utility bills and bank statements serve as secondary verification to confirm address information during customer due diligence. Birth certificates and social security cards are authenticated for higher-risk products, including business accounts. Financial institutions maintain document libraries containing security features for over 10,000 document types issued globally.

Why Is Document Authentication Critical for Banks?

Banks face existential threats from fraud schemes exploiting weaknesses in manual document review. Document authentication protects institutions from regulatory penalties exceeding USD 60 million annually per institution for compliance failures. The technology prevents criminal organizations from establishing accounts using fabricated or stolen identities that facilitate money laundering.

Automated authentication reduces operational costs by eliminating up to 75% of manual document reviews requiring specialized training. Risk mitigation strategies built on document authentication prevent reputational damage from publicized fraud incidents, eroding consumer trust. These systems create audit trails documenting every authentication decision, ensuring banking compliance requirements are satisfied during regulatory examinations.

How Does It Help Prevent Fraud and Identity Theft?

Synthetic identity fraud uses fabricated identities created by combining real and fake information to establish credit profiles undetectable through traditional checks. Synthetic identity fraud causes USD 30-35 billion annual losses in financial services. Americans lost USD 12.5 billion to fraud in 2024 through schemes targeting weak identity verification during account opening.

Cybercrime losses are projected to reach USD 21 billion in 2025 as fraudsters adopt generative AI tools to create convincing counterfeit documents. Document authentication disrupts these schemes by detecting anomalies invisible to human reviewers, including microprint inconsistencies and template mismatches.

What Regulatory Requirements Does It Support?

e-KYC refers to electronic Know Your Customer verification processes mandated by banking regulators to prevent financial crime. The average KYC compliance cost per financial institution is USD 60 million annually due to manual review requirements and regulatory complexity. 99% of institutions report increased compliance costs as regulators demand enhanced due diligence.

Document authentication satisfies requirements under the GLBA by verifying customer identities during account establishment and ongoing monitoring. FACTA Red Flag Rules require institutions to implement programs to detect identity theft indicators, including suspicious document submissions. Automated authentication ensures regulatory audit readiness by creating immutable logs of every verification decision and associated confidence scores.

How Does It Enhance Customer Trust and Security?

Every USD 1 invested in fraud prevention prevents USD 3-5 in losses by blocking fraudulent accounts before funds are disbursed. This return on investment demonstrates how proactive authentication protects institutional assets and customer accounts from unauthorized access. Customers increasingly expect seamless yet secure onboarding experiences that verify identity without requiring branch visits.

Banks deploying document authentication report higher customer satisfaction scores due to faster approval times and reduced false positives. Transparent communication about security protocols builds trust, particularly among demographics concerned about data breaches.

How Does Document Authentication Compare to Other Verification Methods?

Document authentication addresses static identity proof by verifying that government-issued credentials contain authentic security features and match applicant-provided information. Biometric verification confirms the person presenting documents is the rightful owner through facial recognition and fingerprint analysis. AI-powered verification solutions orchestrate multiple authentication methods into unified workflows, balancing security with operational efficiency gains.

Each verification method addresses specific fraud vectors, requiring banks to deploy multimodal approaches layering multiple technologies. Identity authentication overview frameworks recommend combining document verification with biometric and behavioral analysis to achieve acceptable fraud detection rates. Reliance on single verification methods creates exploitable gaps that criminals identify and exploit.

What Are the Differences Between Document Authentication and Biometric Verification?

Biometric inheritance-based authentication uses physiological characteristics like fingerprints that remain constant throughout an individual's lifetime. Knowledge-based authentication relies on passwords and PINs that can be forgotten, stolen, or socially engineered. Fingerprint scanners analyze ridge patterns unique to each individual, comparing submitted prints against stored templates.

3D depth sensing tracks micro-movements for biometric liveness checks that detect presentation attacks using photographs or video recordings. 86% of users prefer biometrics over passwords due to convenience and elimination of credential memorization. Biometric verification complements document authentication by confirming that the person presenting verified documents is the legitimate owner.

How Do AI-Powered Verification Solutions Complement Document Authentication?

Behavioral risk scoring based on user patterns identifies anomalies in account access times, transaction velocities, and device fingerprints. PayPal's AI system blocks USD 500 million in fraud per quarter by analyzing behavioral signals invisible to rule-based systems. Sophisticated fraud patterns emerge when AI systems correlate seemingly unrelated data points across millions of transactions.

AI enhances document authentication by learning new forgery techniques from rejected submissions and updating detection algorithms in real time. Machine learning models identify correlations between document anomalies and subsequent fraudulent activity, enabling preemptive blocking of suspicious accounts. These systems reduce false positives by 40% compared to static rule-based authentication.

What Are the Strengths and Limitations of Each Method?

Document authentication requires high-quality image capture with sufficient resolution to analyze microprint and security features accurately. Systems struggle with damaged or worn documents where security features have degraded through normal use. Less effective against sophisticated state-sponsored forgeries that replicate security features using specialized equipment.

Higher false acceptance rates for certain demographics in facial recognition occur when training data lacks diversity. Environmental factors affect biometric system accuracy, including lighting conditions, camera angles, and background interference. Multimodal verification combining document authentication with biometric and behavioral analysis mitigates individual method limitations while maintaining an acceptable user experience.

What Are Consumer Preferences Regarding Document and Identity Verification?

Consumers prioritize verification processes, balancing security with convenience, rejecting systems requiring excessive steps or repeated submissions. Survey data reveals 70% of users prefer biometric authentication to password-based systems due to speed and elimination of forgotten credentials. Banks balancing fraud prevention with customer acquisition must design authentication workflows completing verification within 60-90 seconds to prevent abandonment.

Generational differences create divergent expectations, requiring institutions to offer multiple verification pathways accommodating varying technology comfort levels. Younger demographics accept biometric scanning and AI-powered verification as standard security measures, while older customers prefer traditional document submission methods.

How Do User Expectations Influence Verification Technologies?

70% of mobile banking users across six nations use facial login as their primary authentication method. 81% of smartphones had biometrics enabled as of 2022, establishing consumer expectations for similar authentication options across all digital services. 75% of US consumers have used biometric tools, including fingerprint scanners, facial recognition, or hand geometry verification.

These adoption rates demonstrate consumer acceptance of advanced authentication methods when properly implemented with transparent privacy disclosures. Banks investing in identity authentication systems meet customer expectations while achieving superior fraud detection compared to legacy password-based systems. Mobile-first authentication strategies align with consumer preferences for completing financial transactions entirely through smartphone applications.

How Do Generational Differences Affect Adoption?

Millennials are 32% more likely to enable two-factor authentication after a data breach compared to 28% of the general population. This heightened security awareness drives the adoption of advanced verification methods, including biometric scanning and push notification approvals. Only 5% of Boomers are interested in AI-driven commerce compared to 30% of Millennials who embrace automated verification.

Banks must design verification systems accommodating these generational preferences without creating security gaps. Older customers benefit from hybrid approaches offering both traditional document upload and in-branch verification alongside digital-first options. Educational initiatives explaining authentication benefits and privacy protections increase adoption rates among demographics initially resistant to biometric technologies.

What Are the Key Factors Consumers Consider in Verification Processes?

Consumers prioritize convenience and ease of use, favoring verification processes completing account opening within single sessions without follow-up documentation. Fraud protection ranks as the primary factor in North America and Europe, where data breach awareness drives security consciousness. Perceived value, including better benefits, lower fees, and fair pricing, remains consistent across regions.

Speed of verification directly impacts account opening completion rates, with every additional authentication step reducing conversion by 15-20%. Transparency about data usage and storage addresses privacy concerns, preventing customers from completing biometric enrollment. Mobile optimization ensures verification processes function identically across devices.

How Is Document Authentication Implemented in Banking Operations?

Banks implement document authentication through API integrations, connecting core banking systems to specialized verification service providers offering global coverage. Cloud-based deployment models eliminate infrastructure requirements while providing automatic updates to document templates and fraud detection algorithms. On-premise installations serve institutions with data residency requirements or legacy systems incompatible with cloud connectivity.

Integration approaches vary based on verification volume, with high-volume institutions negotiating enterprise licensing agreements covering unlimited monthly verifications. Smaller banks utilize pay-per-verification pricing aligned with actual usage. Hybrid models combine baseline licensing fees with per-verification charges above predetermined thresholds.

What Are Common Integration Approaches and Pricing Models?

Document authentication ranges from USD 0.50-8.00+ per verification, depending on tier, feature set, and contracted volume. Low-volume pricing of USD 3.00-8.00 per verification applies to institutions processing fewer than 10,000 verifications annually. Mid-volume pricing of USD 2.00-5.00 per verification serves banks processing 10,000-100,000 verifications annually.

Enterprise volume pricing of USD 0.75-2.00 per verification rewards institutions processing more than 500,000 verifications annually. Implementation fees range from USD 5,000 for basic API integration to USD 50,000+ for enterprise deployments requiring custom workflows. Additional costs include AML watchlist screening at USD 0.50-2.00 per check and ongoing identity monitoring.

How Do Banks Balance Security with User Convenience?

Banks implement progressive verification where initial document checks occur during account opening, with enhanced verification triggered by suspicious activity. This approach minimizes friction for legitimate customers while maintaining security controls appropriate to transaction risk levels. Risk-based authentication adjusts verification requirements based on account value, transaction size, and customer behavioral history.

Mobile-optimized verification workflows enable customers to complete document submission through smartphone cameras without scanning equipment. Clear instructions with real-time feedback guide customers through optimal document positioning, reducing rejection rates from poor image quality. Automated quality checks immediately identify inadequate submissions, allowing customers to resubmit before abandoning the process.

What Are Examples of Successful Document Authentication Use Cases?

Jumio specializes in AI-powered KYC and multi-modal biometrics for enterprise BFSI and gaming sectors requiring high-assurance verification. Onfido offers facial recognition and document verification optimized for fintechs and marketplaces, prioritizing speed and mobile-first experiences. Socure focuses on AI fraud prevention and synthetic identity detection with risk scoring calibrated for financial services.

ID.me dominates the government identity sector with 152 million verified users across federal and state agency implementations. Uber implemented penny drop verification to reduce payment fraud false positives by requiring users to confirm small authorization amounts, successfully reducing customer service tickets while maintaining fraud prevention effectiveness.

What Are the Emerging Challenges and Innovations in Document Authentication?

Deepfake technology enables criminals to create convincing fake videos impersonating legitimate customers during video verification sessions. Detection systems must evolve continuously as generative AI tools become more accessible and sophisticated in replicating human characteristics. Banks face escalating investments in counter-deepfake technology as fraudsters leverage the same AI advances powering legitimate authentication improvements.

Liveness detection prevents presentation attacks where criminals present photographs or video recordings instead of appearing live during biometric capture. Privacy regulations, including GDPR, create compliance obligations for biometric data storage and processing that vary significantly across jurisdictions. These challenges require banks to maintain flexible authentication frameworks accommodating regional regulatory differences.

How Does AI Address Emerging Fraud Tactics Like Deepfakes?

Deepfakes are AI-generated fake videos or images that mimic real people with sufficient realism to fool human reviewers. Deepfakes are linked to 1 in 5 biometric fraud attempts as criminals deploy these tools against video-based identity verification. A 4,151% surge in deepfake-related fraud incidents demonstrates the escalating threat requiring advanced AI countermeasures.

ID.me blocked 75 million deepfakes and prevented over USD 270 billion in potential fraud through neural networks trained on deepfake detection. These systems analyze micro-expressions, lighting inconsistencies, and pixel-level artifacts invisible to human reviewers. Hardware-based liveness detection using device sensors provides additional verification layers confirming physical presence during authentication sessions.

What Role Does Liveness Detection Play in Enhancing Document Checks?

Document liveness detection prevents presentation attacks using screens or printed copies of previously verified documents. 3D depth sensing tracks micro-movements for biometric liveness checks that distinguish live subjects from photographs or recordings. Presentation attacks using screens or printed document copies are defeated through texture analysis, identifying digital display characteristics.

Need for robust liveness checks to prevent spoofing drives adoption of hardware-enabled verification using smartphone sensors, including accelerometers and infrared cameras. Challenge-response protocols require users to perform random movements like head turns or eye blinks impossible to replicate with static media. These techniques combine with document authentication to create layered defenses preventing criminals from bypassing individual security controls.

How Are Privacy and Compliance Considerations Managed?

Complex data privacy regulation compliance challenges arise from biometric data's classification as sensitive personal information under GDPR and similar frameworks. Algorithmic bias risks in AI systems create legal exposure when verification systems exhibit disparate impact across protected demographic categories. Banks must conduct regular bias audits and maintain diverse training datasets, ensuring equitable performance.

Data minimization principles require banks to collect only the biometric data necessary for authentication, deleting samples immediately after verification completion. Consent management systems provide customers with granular control over biometric data collection and storage with clear opt-out mechanisms. Encryption of biometric templates both in transit and at rest protects against data breaches.

How Does Document Authentication Fit into a Broader Fraud Prevention Strategy?

Document authentication serves as the foundational layer in defense-in-depth strategies, layering multiple verification technologies addressing different fraud vectors. Effective fraud prevention requires orchestrating document checks with transaction monitoring, device fingerprinting, and behavioral analytics into unified risk scores. No single technology eliminates fraud entirely, requiring banks to deploy complementary systems that compensate for individual method limitations.

Integration with case management systems enables fraud analysts to review flagged verifications within workflows, consolidating document images, risk scores, and transaction histories. Automated decisioning rules approve low-risk verifications instantly while routing suspicious submissions for manual review. This balanced approach maintains operational efficiency gains while ensuring human oversight for edge cases requiring judgment beyond algorithmic capabilities.

What Is the Role of Multimodal Verification in Banks?

Multimodal verification combines document authentication with biometric and behavioral analysis to create comprehensive identity assurance across customer lifecycles. Banks verify documents during account opening, then authenticate subsequent logins using facial recognition or fingerprint scanning without requiring repeated document submission. Continuous authentication monitors behavioral patterns, including typing cadence and mouse movements, to detect account takeover attempts.

Layered security prevents credential stuffing attacks, where criminals use stolen passwords to access accounts protected by biometric re-authentication requirements. Transaction risk scoring triggers step-up authentication requiring additional verification when unusual activity patterns emerge. This dynamic approach balances security with user experience by applying friction proportionate to detected risk levels.

How Does Document Authentication Reduce False Positives?

Penny drop verification requires users to confirm small authorization amounts to prove payment method ownership when document checks produce inconclusive results. False positives can restrict legitimate users, creating a customer service burden and account abandonment. Document authentication reduces false positives by analyzing multiple document features simultaneously rather than relying on single-factor checks prone to errors.

AI-powered systems learn from analyst feedback on flagged verifications, automatically adjusting detection thresholds to minimize incorrect rejections while maintaining fraud detection rates. Confidence scoring enables banks to accept verifications exceeding high-confidence thresholds automatically while routing borderline cases for human review. This approach reduces manual review volume by 60-70% compared to systems lacking sophisticated scoring algorithms.

What Is the ROI of Investing in Document Authentication?

Every USD 1 invested in fraud prevention prevents USD 3-5 in losses by blocking fraudulent accounts before criminals conduct unauthorized transactions. This return on investment compounds over time as fraud scales with transaction volume growth without proportional security investment increases. Avoiding compliance penalties from regulatory failures due to inadequate KYC controls provides additional ROI beyond direct fraud prevention savings.

Operational efficiency gains from automated verification reduce labor costs associated with manual document review. Customer acquisition costs decline when streamlined verification processes improve account opening completion rates by reducing abandonment. These combined benefits typically generate positive ROI within 6-12 months for institutions processing more than 5,000 verifications monthly.

The Strategic Importance of Document Authentication for Banks

The global identity verification market is projected to grow from USD 14.34 billion in 2025 to USD 29.32 billion by 2030. Market CAGR of 15.4% from 2025-2030 reflects accelerating adoption driven by escalating fraud threats and regulatory pressure. Long-term projection of USD 50.58 billion by 2034 with 15.60% CAGR demonstrates sustained market expansion.

The US market is projected to reach USD 8.16 billion by 2030 from USD 4.34 billion in 2025 as domestic banks upgrade legacy verification systems. North America holds 38.4% market share due to regulatory mandates and government digital identity initiatives. These market dynamics position document authentication as a strategic infrastructure investment rather than a discretionary security enhancement.

Banks implementing comprehensive authentication frameworks protect institutional assets while satisfying evolving regulatory expectations for customer due diligence. The convergence of AI-powered verification, biometric authentication, and behavioral analytics creates defense systems outpacing criminal innovation. Financial institutions delaying authentication modernization face competitive disadvantages as customers migrate to banks offering superior security with better user experiences.

Don't Wait for Fraud to Reach Your Bank

Counterfeit IDs, synthetic identities, and deepfake submissions slip past manual review every day. One missed verification can cost your institution six figures in fraud losses, regulatory fines, and customer trust that takes years to rebuild.

FraudFighter has protected financial institutions for over 25 years — including Wells Fargo, Capital One, and thousands of community banks and credit unions. Our SOC 2 Type II–compliant document authentication platform verifies identity documents in under 10 seconds, supports BSA, CIP, and FACTA Red Flag Rule compliance, and trains any teller in minutes.

One credit union used FraudFighter to stop a single $43,000 fraud attempt — paying for the system many times over before the next month closed. Schedule a free consultation with FraudFighter and see exactly where fraud is entering your branch — before it shows up on your next audit. Most member-facing teams pair that review with a countertop ID scanner at the new-accounts window, catching a forged license the moment it lands in a teller's hands.