The Future of the U.S. Dollar & How it Might Affect Your Business

It is often said that the act of counterfeiting money is as old as money itself. No matter the type of currency used throughout history – whether it was the metal coins used in Lydia in 640BC or the cowry shells that were used as currency in Orissa, India until 1805 – there was sure to be someone intentionally attempting to pass off a counterfeit version as the real thing.

Ever since its inception, the United States has been brimming with counterfeiting activity. In fact, counterfeiting has been prevalent and commonplace throughout US history - so much so that, during the US Civil War - it is estimated that a third of all currency in the United States was counterfeit. This, in turn, led the formation of the US Secret Service by order of President Lincoln.

To combat counterfeiting, the answer has always been to redesign currency to make it more secure. In the United States, redesigned bills will be entering circulation sometime in the next decade.

The Upcoming Redesign of US Currency

The US Treasury has announced that the $5, $10, and $20 bills will all be redesigned. The purposes of the redesign are two-fold:

- to feature a more comprehensive history of America

- to make US money harder to counterfeit

Both purposes are good reasons to redesign the bill: one addresses a social aspect and the other addresses a financial aspect.

The redesign based on social reasons means that images and text on the bills will be historically and aesthetically enhanced. In other words, the goal is to make the historical highlights on the bills as visually appealing as possible. After all, who wants unsightly bills representing their country’s currency?

And the redesign based on financial needs means that the new bills most likely be enhanced with up-to-date security features. These up-to-date security features – discussed below – indeed will make it harder to counterfeit. If the security features on bills are harder to counterfeit in such a way they can pass for real money, the going theory is that criminals simply won’t counterfeit money because it’s simply not lucrative enough anymore.

“What you’re trying to do is create a banknote that’s very difficult to forge, either in being costly, or in effort. If someone has to go through a huge amount of effort to reproduce these to pass it, it’s not going to be a cost-effective proposition. If we make it just too difficult for them, they’re just not going to be tempted.”

For businesses, having currency that is much harder to counterfeit should provide some relief from worrying about fraud. Counterfeit money will be much less likely to financially hurt businesses. But this relief is about ten years away. The redesigned bills with updated security features are not scheduled to be released for another decade or so, at a date that is still yet to-be-determined by the US Federal Reserve.

Although the new designs haven’t been released, much less finalized, we can predict with relative confidence what the new security features on the bills will be. To get an idea of what we can expect from redesigned US bills, we should take a look at Australia.

Australia Releases its New $5 Bill

Australia released a new $5 with a design primarily based on thwarting counterfeiters, with other redesigned denominations to be released in the coming years. Commenting on the release of the new $5 bill, the Reserve Bank of Australia Assistant Governor, Michele Bullock, said, “The reason for doing this now is to just make sure that we are staying well ahead of the counterfeiters.”

Below is a brief overview of the emerging, cutting-edge security features on the new Australian $5 bill that are not present on US currency.

Currency Security Features of the Future (based on the new Australian $5):

Polymer Substrate: Polymer is a type of plastic and has a distinctive feel. Even after being scrunched up, it should return back to its original shape (Although Australia started using bills made from polymer 25 years ago, this is not yet a feature of US currency)

Clear Top-to-Bottom Window: The clear top-to-bottom window - about a fifth of the bill’s width - that has multiple security features, and is an integral part of the banknote, not an addition (This security feature is a world first on money)

Rolling Color Effect: Tilting the banknote causes certain images to have a “rolling” rainbow color effect

“Moving” Hologram: Holograms that “move” based on the angle

There are also other security features that not publicly listed, for obvious, security reasons. These undisclosed security features are what the government, banks, and other official entities use to make sure that money is real.

Cash is Still King

As much as it seems like the world is conducting the majority of its transactions using electronic means these days, 85% of transactions are actually still conducted using cash. Although some may consider cash too cumbersome and annoying to carry around and use, the majority of people still use cash for at least some of their transactions. The reason behind this is a matter of comfort: Cash is convenient, private, and intuitive. Quite simply, people trust cash.

Almost all cash-alternative options for transactions – credit cards, Apple Pay, Google Wallet – have fees affixed to them. Some merchants pass off that fee to their customers, some don’t. Either way, someone has to pay these fees for electronic transactions – fees that are not present at all for cash transactions.

In the electronic arena, the most promising cash-alternative option has been Bitcoin. Bitcoin, to put it simply, places all Bitcoin information – transactions, users, Bitcoin account amounts – as bits and pieces on private servers all over the world, which, in theory, makes the data inviolable; that Bitcoin is free from fake data. But yet many are still incredibly skeptical that Bitcoin is the answer to a cash-free world. As Nathaniel Popper, a finance and technology reporter for The New York Times wrote: “Bitcoin itself is always one big hack away from total failure.”

The Potential Effects of New Currency on Businesses

Although redesigning US currency to have updated security features can definitely deter counterfeiting, or at least, the counterfeiting of passable bills, it can potentially have unintended consequences that can actually ramp up counterfeiting attempts. Consider the following:

It is incredibly important to keep in mind that new currency entering circulation does not mean that the old currency is suddenly invalid.

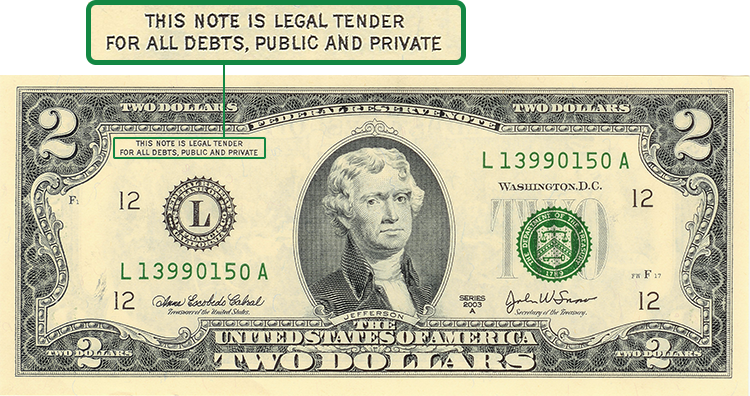

Take the case of the schoolgirl who tried to pay for her lunch using an old $2 bill, which had a design that the cashier did not recognize. Although the $2 bill was so old that it misled an adult to believe that the bill was counterfeit, the $2 bill was still legal tender.

All real money is legal tender until it is physically taken out of circulation by the either the US Bureau of Engraving and Printing, the same government entity that is responsible for printing the money in the first place, or the Federal Reserve, the government entity that is responsible for distributing the money.

Redesigned bills entering the circulation does not mean that businesses can choose to no longer accept bills with the previous design anymore; those old bills are still considered legal tender.

Knowing that a more difficult to counterfeit bill will soon be the standard, it is highly probable that criminals will escalate their attempts to spend counterfeit bills with the old design, which will be incredibly unfortunate for businesses, especially retail businesses.

It’s already a phenomenon that analysts have been noticing, but enterprising criminals have been in increasing numbers moving their fraudulent activities into the electronic world by committing identity theft.

To make a long story short, criminals who are behind data breaches more often than not sell the identity data that they have stolen on the dark web to other criminals who then use that data to use those identities to commit financial fraud, whether it’s by opening new credit card accounts, manipulating existing accounts, or some other means. New credit card accounts can even be supplemented by fraudulent identity documents, such as a driver license, assuaging any suspicions that cashiers or tellers may have.

Taking away an avenue for fraudulent activity – the ability to spend passable counterfeit money – means that criminals will find another avenue to achieve the same results. And once fraudulent activity moves to the electronic environment, the impact on businesses will be considerable.

Counterfeiters do not spend counterfeit money to simply receive goods for free – they use the counterfeit money to make low-cost purchases from which they receive real money in return as change. Since change isn’t given from electronic transactions, criminals are simply making large, expensive purchases to maximize their return on investment. In essence, fraudulent electronic transactions translate to greater losses per transaction than fraudulent cash-based transactions.

The above potential consequences are further exacerbated by the amount of time it will take to release currency with updated security features – at least 10 years – means that criminals have ample time to prepare and take advantage. If you were a criminal and knew that there was an upcoming change to currency that will make it harder for to make counterfeit money, wouldn’t you double, triple, quadruple, your efforts to spend as much counterfeit money until the new money is released? And once the new currency is released, wouldn’t you move your fraudulent activities to the electronic environment where there is less friction?

To be fair, however, the process of redesigning currency can be a bureaucratic nightmare. In fact, it took the Australian government around 10 years to place their new $5 bill into circulation, which is roughly the amount of time it will take to redesign the upcoming US bills.

Your business shouldn’t experience any more counterfeiting instances than before for the immediate future. But in the coming years, you can be sure to expect more counterfeiting instances in your stores - by criminals paying with either fake money or fraudulent electronic means - and subsequently, the proportional effects of counterfeiting on your profits. And once the new money is actually released into circulation, you can be sure that counterfeiting attempts will continue, especially by using counterfeit money based on the previous bill designs.

The one, sure positive effect that the new bills have will be that businesses can be confident accepting the new bills as real money: in comparison to the bills we have now, they will unquestionably be harder to counterfeit.

However, just like with any other redesign of money, it will only be a matter of time until criminals figure out how to create a passable, counterfeit US bill. We are at that point in time now - which is why the United States is currently in the midst of redesigning money.

When the current designs were released – the last one being 2008 with the $5 bill – criminals didn’t just figure out how to effectively counterfeit bills overnight. But fast-forward to today, and criminals all over the world have figured out how to make counterfeit money production so cost-effective that those previously in the drug trade are turning to counterfeit money production because it is more lucrative.

And once criminals figure out how to counterfeit the upcoming redesigned bills, we’ll be right back where we are already, giving the criminals another decade or so of a counterfeiting free-for-all while new, more securely designed money is developed.